Traveling opens doors to new experiences, but it also exposes you to unexpected health risks. Medical insurance for traveling provides essential protection against costly emergency medical expenses when you’re away from home. Without proper coverage, a simple injury or illness abroad could cost thousands of dollars, potentially derailing your trip and finances. This comprehensive guide explains everything you need to know about travel medical insurance, helping you make informed decisions for safe and worry-free travels in 2025.

What Is Travel Medical Insurance?

Travel medical insurance is a specialized insurance policy that covers emergency medical expenses and related services when you’re traveling outside your home country. Unlike your regular health insurance, which may offer limited or no coverage internationally, travel medical insurance is specifically designed to protect you from the high costs of healthcare abroad.

This type of insurance typically covers emergency medical treatments, hospital stays, prescription medications, and emergency medical evacuations. It provides peace of mind knowing that if you face a medical emergency while traveling, you won’t have to bear the financial burden alone.

According to the World Health Organization, millions of travelers require emergency medical assistance while abroad each year, with costs often ranging from several thousand to hundreds of thousands of dollars for severe conditions requiring evacuation.

✅ Key Takeaways: What Is Travel Medical Insurance?

- Specialized Protection Abroad:

Travel medical insurance is specifically designed for travelers and covers medical emergencies that your regular health insurance may not cover internationally. - Coverage Includes:

- Emergency medical treatment

- Hospitalization

- Prescription medication

- Emergency medical evacuation

- Why It Matters:

Your home health insurance often won’t cover you abroad, and hospital bills overseas can easily reach six figures, especially for airlift or ICU services. - Peace of Mind for Global Travel:

Travel medical insurance provides you with financial security and access to quality care, wherever you are in the world. - Real Stats:

The World Health Organization reports that millions of travelers require emergency medical assistance abroad each year, and without coverage, many are left with substantial bills.

🧠 Useful Facts to Highlight

- Your U.S. health plan (even premium ones) typically does not cover international care, or it covers it reimbursably with significant delays.

- Evacuations (especially from remote areas or islands) can cost between $25,000 and $ 250,000, depending on the location and mode of transport.

- Many hospitals require upfront payment from foreigners who do not provide travel medical insurance.

📚 Must-Reads Before You Travel for Treatment

- 📘 The Complete Handbook to Medical Tourism

Break down costs, compare destinations, and avoid scams with this deep-dive guide.

👉 Read it now.» - 🛡️ Ultimate Travel Insurance Guide for U.S. & Global Travelers (2025)

Understand what your policy covers and how to avoid hidden exclusions.

👉 Explore the guide » - 📊 2025 Travel Insurance Report

Compare top-rated plans, insider tips, and must-know changes in the travel insurance space.

👉 View the report.»

Who Needs Medical Insurance for Traveling?

While travel medical insurance is beneficial for most international travelers, certain groups have a greater need for this protection. Understanding your specific situation will help determine the level of coverage required.

Leisure Travelers

Vacationers traveling internationally need coverage, as domestic health insurance typically does not extend beyond national borders. Even short trips can expose you to unexpected medical emergencies.

Medical Tourists

Those traveling specifically for medical procedures need specialized coverage that addresses complications, extended stays, and follow-up care related to their treatment.

Digital Nomads

Long-term travelers working remotely often require continuous medical coverage across multiple countries, necessitating renewable or long-term insurance solutions.

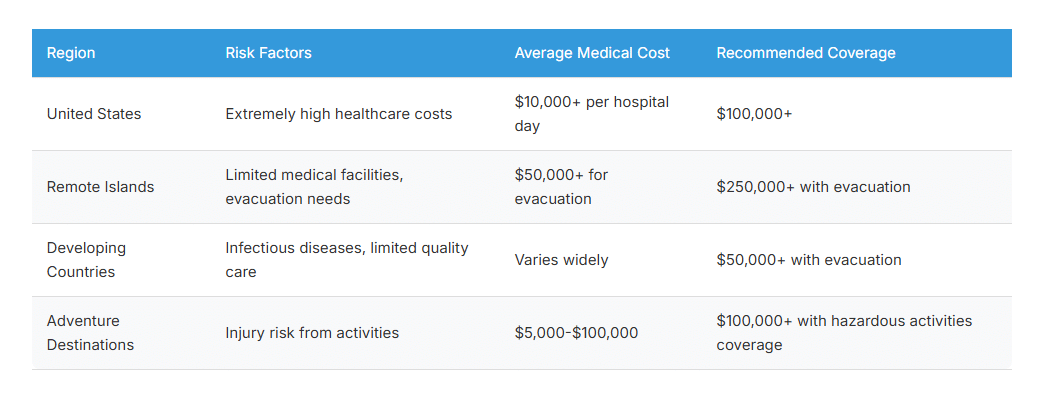

High-Risk Destinations

Some destinations pose greater health risks or have extremely high medical costs, making travel medical insurance particularly important:

🩺 Travel Medical Insurance Coverage Explained

Travel medical insurance is designed to cover emergency health-related costs while you’re outside your home country, especially in regions where your primary health insurance doesn’t apply. Here’s a breakdown of what’s typically covered, what’s optional, and how it works:

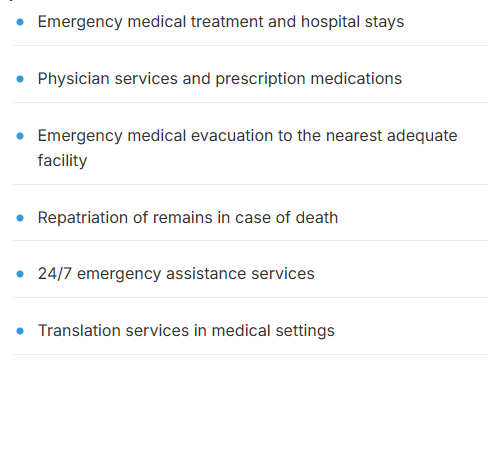

✅ What’s Typically Covered

| Coverage Type | What It Means |

|---|---|

| Emergency Medical Treatment | Covers hospital visits, doctor fees, diagnostic tests, and prescription medication due to unexpected illness or injury. |

| Emergency Evacuation | Covers the cost of air ambulance or transport to the nearest adequate medical facility. Critical for remote destinations. |

| Hospital Stays | Includes overnight care, ICU admission, surgical procedures, and in-patient services. |

| Repatriation of Remains | Pays for the transport of remains to your home country in the event of death abroad. |

| 24/7 Assistance Services | Toll-free access to multilingual agents who can help with hospital referrals, legal support, and translation. |

⚠️ Optional Add-Ons & Upgrades

| Add-On | Benefit |

|---|---|

| Pre-Existing Condition Waiver | Some plans will cover pre-existing conditions if you meet specific timing requirements. |

| Trip Interruption Coverage | Reimburses prepaid costs if your trip is cut short due to a covered medical event. |

| Adventure Sports Coverage | Required if you’ll be skiing, diving, or participating in high-risk activities. |

| Telemedicine Access | Virtual consults with licensed doctors — helpful for minor ailments or second opinions. |

📌 Real-World Example

Imagine a U.S. traveler on a layover in Thailand who experiences severe abdominal pain. A hospital visit, imaging tests, and minor surgery total $6,000 USD. Without travel medical insurance, they would pay out-of-pocket. With a solid policy, they’d only owe the deductible — often just $50 to $250.

🧠 Things to Check in Your Policy

- Maximum Coverage Limit: Look for coverage of $ 100,000 or more for medical care and $ 250,000 or more for evacuation.

- Deductible Options: Higher deductibles lower your premium, but make sure you can afford them in an emergency.

- Network Access: Some insurers have preferred global hospital networks, which can reduce upfront costs.

- Claim Process: Choose providers with fast online claim filing and English-language support.

🔗 Top Resources & Tools

- SafetyWing Insurance – Monthly subscription insurance for travelers and nomads

- InsureMyTrip – Compare top travel medical plans side-by-side

- World Nomads – Popular with adventurous travelers and backpackers

- CDC Traveler’s Health – U.S. government travel health notices and vaccination advice

- U.S. State Dept Travel Insurance Guide

Standard Inclusions (Recap)

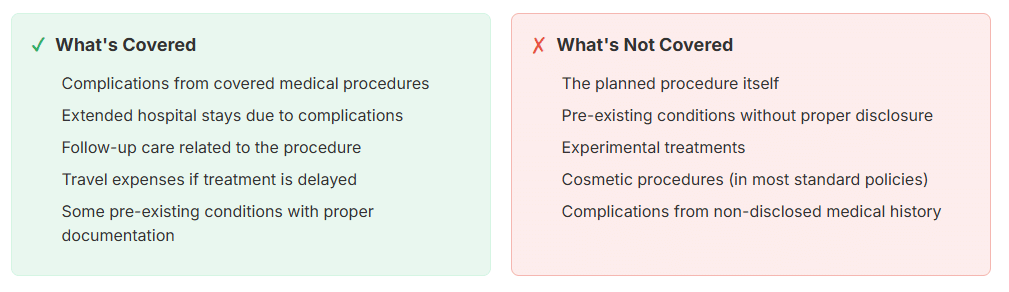

Medical Tourism Specifics

If you’re traveling specifically for medical procedures, standard travel medical insurance may not be sufficient. Medical tourism insurance offers specialized coverage:

COVID-19 and Pandemic Coverage

Since the COVID-19 pandemic, many travel medical insurance policies have adapted to include coverage for pandemic-related illnesses. When selecting a policy, verify:

Top Travel Medical Insurance Providers Compared

We’ve analyzed the most popular travel medical insurance providers to help you compare your options:

| Provider | Cost Range | Key Features | Medical Tourism Support | Best For |

| Allianz | $40-$120/week | Strong emergency assistance network, user-friendly app | Limited | General travelers, families |

| World Nomads | $35-$110/week | Adventure activities coverage, flexible plans | No | Adventure travelers, backpackers |

| IMG | $25-$95/week | High coverage limits, long-term options | Yes, with specific plans | Expats, medical tourists |

| SafetyWing | $42/4 weeks | Subscription model, renewable coverage | No | Digital nomads, long-term travelers |

| GeoBlue | $50-$150/week | Blue Cross network, premium service | Yes, comprehensive | Business travelers, medical tourists |

- COVID-19 testing and treatment coverage

- Quarantine expense coverage if you test positive

- Trip interruption benefits for pandemic-related issues

- Coverage for new variants and emerging health threats

- Vaccination requirements for coverage validity

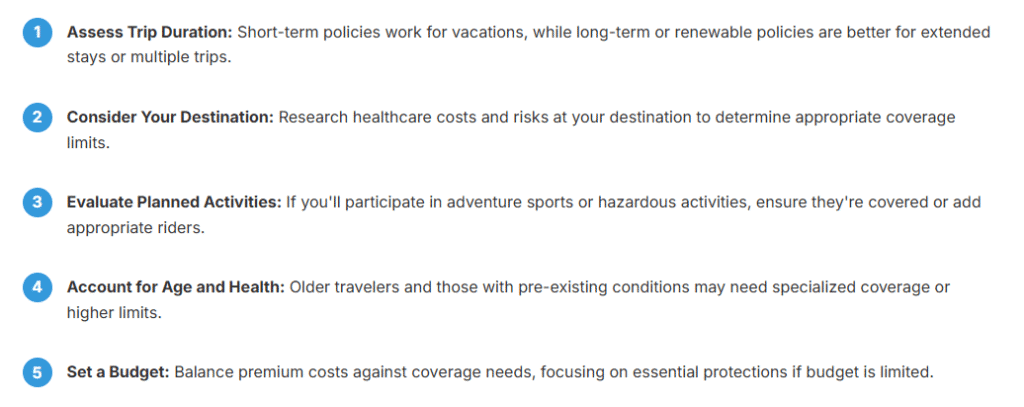

Choosing the Right Medical Insurance for Traveling

Selecting the appropriate travel medical insurance requires careful consideration of several factors. Follow this 5-step checklist to find the best coverage for your needs:

Before you board that flight, make sure you’ve packed everything — from medical records to emergency contacts. Our free Medical Travel Checklist helps you stay safe, organized, and stress-free.

Which countries require travel medical insurance for entry?

Common Exclusions and Red Flags in Travel Medical Insurance

Even the best travel medical insurance plans come with limitations, exclusions, and fine print. Understanding these ahead of time can save you from unexpected bills, denied claims, and avoidable stress and misunderstandings abroad.

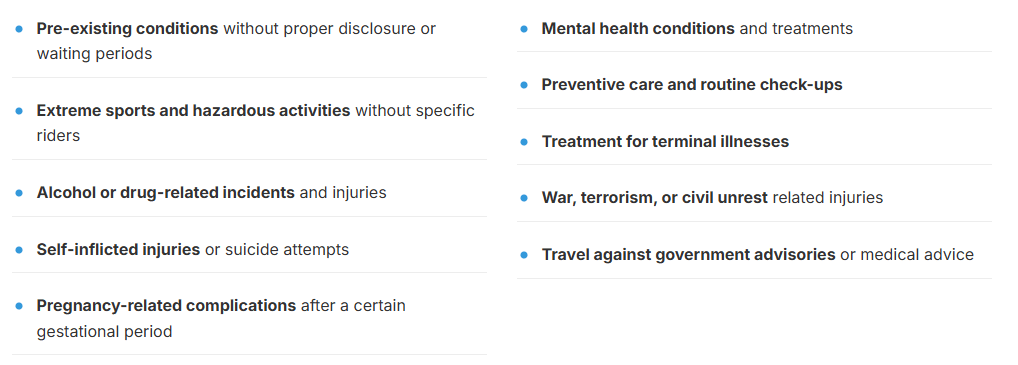

🔍 1. Pre-Existing Conditions

Most standard travel medical insurance plans exclude coverage for pre-existing conditions, including chronic illnesses or recent surgeries. Some policies offer a waiver, but only if you meet strict conditions (such as purchasing within 10–14 days of booking your trip).

🧳 2. High-Risk Activities

Adventure travel? Think again. Many policies do not cover injuries sustained while:

- Skydiving

- Scuba diving

- Rock climbing

- Riding a motorcycle without a license or helmet

If your layover includes high-adrenaline activities, you’ll need a policy that explicitly includes coverage for adventure sports.

💊 3. Routine or Elective Care

Travel medical insurance is designed for emergencies, not routine checkups. This means:

- No coverage for dental cleanings, eye exams, or cosmetic treatments

- Elective procedures (unless pre-authorized for medical tourism) are typically not reimbursed

✈️ 4. Traveling Against Medical Advice

If you travel while medically unfit, many insurers can deny claims. This includes:

- Traveling while pregnant past a specific term (often 26–28 weeks)

- Ignoring medical advice to stay home

- Booking travel right after surgery without clearance

🛑 5. Alcohol or Drug-Related Incidents

Any injury or illness related to alcohol or drug use is almost always excluded, including:

- Accidents while intoxicated

- Hospitalizations after alcohol poisoning

- Medication misuse or non-prescribed drugs

🔎 Red Flags to Watch Out For:

- No direct billing with hospitals abroad (you pay first, file later)

- High deductibles or unclear copays

- Coverage limits that cap emergency evacuations

- No 24/7 emergency hotline or slow claims support

10 Common Exclusions to Watch For (Recap)

Warning: Beware of “Too Good to Be True” Policies

Extremely cheap travel medical insurance often contains significant coverage gaps or high deductibles. Watch for these red flags:

- Unusually low coverage limits (under $25,000 for emergency medical)

- Excessive exclusions or vague policy language

- Requirement to pay upfront for all medical costs

- No 24/7 emergency assistance hotline

- Poor reviews or unresolved complaints

💉 Can You Buy Medical Travel Insurance for These Procedures?

Not all medical travel insurance plans are created equal, and coverage varies wildly depending on the nature of the procedure. While emergency care is always the baseline, elective and pre-planned procedures require more nuance.

🦷 Basic or Elective Procedures (Usually Not Covered by Default)

| Procedure | Covered by Insurance? | Notes |

|---|---|---|

| Teeth Cleaning | ❌ Not covered | Considered routine dental care. Not classified as medically necessary. |

| Botox & Fillers | ❌ Not covered | Classified as cosmetic. Exception: Botox for migraines may be covered with documentation. |

| Laser Eye Surgery (LASIK) | ❌ Usually not covered | Elective unless medically necessary for visual impairment. |

| Teeth Whitening / Veneers | ❌ Not covered | Purely cosmetic. However, dental injury repair may be covered under accident insurance. |

🩺 Medically Necessary (May Be Covered with Add-Ons or Specialized Plans)

| Procedure | Covered by Insurance? | Notes |

|---|---|---|

| Dental Implants / Root Canals | ⚠️ Sometimes | Coverage available through travel dental insurance (e.g., HTH, GeoBlue). Pre-approval often required. |

| Hair Transplant (FUE/FUT) | ❌ Not covered | Considered elective and cosmetic. Rare exceptions for trauma-induced hair loss. |

| Weight Loss Surgery (Bariatric) | ⚠️ Limited | Requires pre-authorization. May be covered under specific medical tourism packages. |

| IVF / Fertility Treatments | ⚠️ Limited | Often excluded, but some premium plans or medical tourism bundles offer optional coverage. |

🚑 Advanced or High-Risk Procedures (Often Covered with Medical Travel Insurance)

| Procedure | Covered by Insurance? | Notes |

|---|---|---|

| Orthopedic Surgery (e.g., Knee Replacement) | ✅ Yes | Must be medically necessary. Plans like IMG, Seven Corners, or GeoBlue may cover. |

| Cancer Treatment | Covered if the pre-existing condition clause is met. Consider a major medical travel plan. | Covered if pre-existing condition clause is met. Consider a major medical travel plan. |

| Organ Transplant / Dialysis | ⚠️ Complex | Rarely covered unless arranged by an international hospital network + high-tier plan. |

| Cardiac Surgery (e.g., Bypass) | ✅ With documentation | Covered with prior medical records and coordination through a recognized facility. |

⚠️ Pro Tip:

Most standard travel medical insurance plans do not cover planned or elective procedures. You need either:

- Specialized medical tourism insurance (partnered with clinics)

- Major international health insurance (e.g., Cigna Global, IMG Global Medical)

- Or a dedicated policy rider added for high-risk or high-cost care

🔗 Helpful Resources

- HTH Travel Insurance – Dental & Specialty Medical

- IMG Global Medical Plan

- Seven Corners Travel Medical

- Medical Tourism Association – Look for accredited hospitals with insurance partnerships

✈️ Final Thoughts: Don’t Leave Without It

Whether you’re jetting off for a quick layover in Paris, seeking stem cell therapy in Mexico, or embarking on a medical tourism journey in Thailand, travel medical insurance is your silent lifeline. A single emergency abroad can cost more than your entire trip, and most domestic insurance plans offer little or no international coverage.

Don’t gamble on “hoping for the best.” Be the traveler who plans smarter, protects their health, and avoids five-figure surprises.

With the right policy, you’re not just buying coverage — you’re buying peace of mind.

Frequently Asked Questions About Medical Insurance for Traveling

Does Medicare cover international Travel?

No, Original Medicare (Parts A and B) generally does not cover healthcare costs outside the United States and its territories. There are minimal exceptions, such as if you’re in the U.S. when an emergency occurs, but a foreign hospital is closer than the nearest U.S. hospital. Some Medicare Advantage plans and Medicare Supplement (Medigap) Plans C through G offer limited coverage for emergency healthcare during foreign travel.

How much does travel medical insurance typically cost?

Travel medical insurance typically costs between $40 and $80 for a short trip, although prices vary based on factors such as age, destination, trip length, and coverage limits. For travelers under 50, basic coverage might cost as little as $1-2 per day, while comprehensive coverage for seniors or high-risk destinations can reach $10-15 per day. Long-term policies often offer better value with monthly rates.

Can I buy travel medical insurance if I have pre-existing conditions?

Yes, you can purchase travel medical insurance with pre-existing conditions, but coverage varies by provider. Some insurers offer waivers if you buy the policy within 14-21 days of your initial trip deposit and meet stability requirements (no changes in medication or treatment for 60-180 days). Without a waiver, emergency treatment for pre-existing condition flare-ups typically isn’t covered.

How do I file a claim with my travel medical insurance?

Several countries require proof of travel medical insurance for entry, including Schengen Area countries (with a minimum coverage of €30,000), Cuba, Ecuador, Qatar, Russia, Turkey, the United Arab Emirates, and Antarctica. Additionally, Costa Rica, Aruba, St. Maarten, French Polynesia, and Turks and Caicos have implemented insurance requirements. Requirements change frequently, so always check your destination’s current entry regulations before traveling.

Is travel medical insurance the same as trip cancellation insurance?

No, travel medical insurance and trip cancellation insurance serve different purposes. Travel medical insurance provides coverage for emergency medical expenses and evacuations while traveling. Trip cancellation insurance reimburses non-refundable trip costs if you must cancel for covered reasons. Comprehensive travel insurance packages typically include both types of coverage, as well as baggage protection and travel delay benefits.

Does travel medical insurance cover dental emergencies?

Most travel medical insurance plans cover dental emergencies, but with limitations. Coverage typically applies only to unexpected dental injuries or acute pain relief, not routine care or pre-existing dental issues. Coverage limits are often capped at $200-$500, which is significantly lower than the coverage provided by general medical plans. For extensive dental work, specialized dental travel insurance might be necessary, especially for medical tourism related to dental procedures.

Can I extend my travel medical insurance if my trip gets longer?

Yes, many travel medical insurance policies can be extended if you decide to stay longer, but this must be done before your current coverage expires. Contact your insurance provider directly to request an extension. Some policies have maximum duration limits or may require additional medical questionnaires for longer extensions. For frequent travelers, consider multi-trip annual policies or renewable long-term coverage designed for extended stays.

🧰 Helpful Tools & Next Steps

✅ Get the Medical Tourism Checklist Pack →

Download our free bundle to help you plan safely and confidently.

✅ Compare the Best Travel Insurance Providers →

Find policies with emergency coverage, pre-existing waivers, and hospital networks abroad.

✅ Read the Ultimate Travel Insurance Guide →

A deeper dive into how policies work, what to look for, and common traps to avoid.

✅ Explore Medical Tourism by Destination →

Discover safe clinics, top procedures, and destination-specific insurance tips.

🔗 Credible Sources You Can Reference or Link

These will boost your E-E-A-T and can be cited in footnotes or hyperlinked: